NEMT Billing Explained: From Trip to Paid Claim (2026)

How NEMT billing really works in 2026: the claim lifecycle, why claims get denied, EVV and compliance, and how the right billing software gets you paid faster.

Read more

If you're building a NEMT business plan or shopping policies as an established operator, you've probably already felt the sticker shock. NEMT insurance isn't priced like a personal auto policy — and it shouldn't be. You're transporting medically vulnerable passengers, operating under state Medicaid contracts, and managing drivers whose records directly affect your premiums.

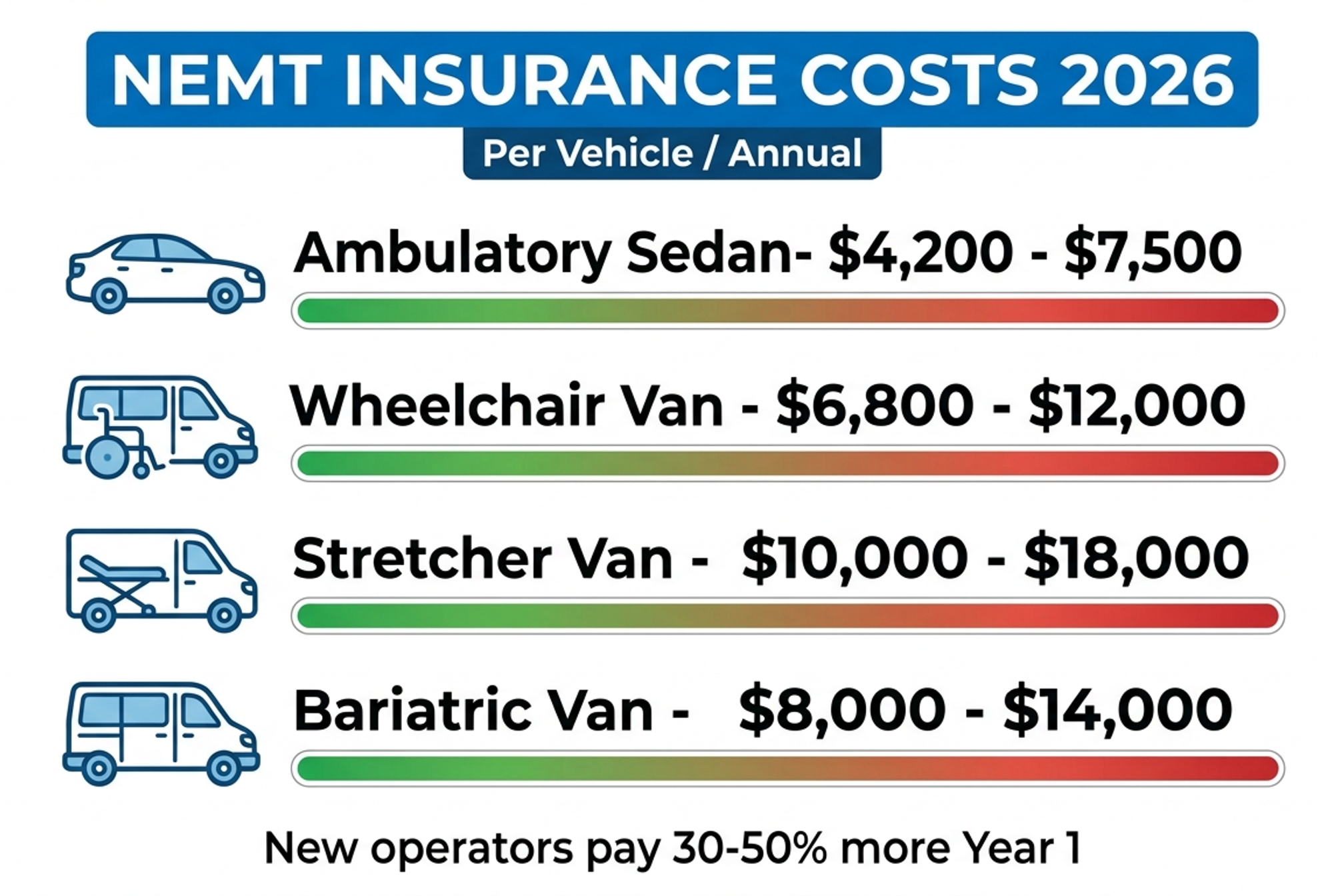

Key Stat: In 2026, the average NEMT operator spends between $8,000 and $22,000 per vehicle annually on insurance, depending on state, fleet size, vehicle type, and loss history. For a five-vehicle fleet, that's up to $110,000 per year in insurance premiums alone — before you hire a single NEMT driver, configure your NEMT billing software, or submit your first trip claim.

This guide breaks down exactly what you'll pay, why costs vary so dramatically, and what the smartest operators are doing to lower premiums without cutting corners on coverage.

Before you can understand cost, you need to understand what you're buying. NEMT insurance is not a single policy — it's a stack of coverages bundled together or purchased separately depending on your broker and state requirements.

This is the foundation of any NEMT insurance program. It covers bodily injury and property damage your vehicles cause to third parties. Most state Medicaid programs require a minimum of $1,000,000 per occurrence in commercial auto liability. Some states require $1.5 million or higher.

This is where NEMT insurance diverges sharply from standard commercial auto. A plumber driving a work van carries commercial auto insurance. But if that van hits a curb, the only injured party is the property. In NEMT, your passengers are medically fragile — stroke survivors, dialysis patients, wheelchair users. A minor accident can result in catastrophic injury claims, and insurers price accordingly.

Commercial auto covers incidents that happen while the vehicle is moving. General liability covers incidents that happen outside the vehicle — a passenger slipping during a transfer, a wheelchair tipping during loading, or an injury at a pickup location. Limits of $1,000,000 per occurrence / $2,000,000 aggregate are standard across most NEMT contracts.

If your NEMT drivers ever use their personal vehicles for company trips — or if you rent vehicles — non-owned and hired auto fills the gap your commercial fleet policy leaves behind.

Required in most states. Protects your passengers and vehicles when the at-fault driver carries insufficient coverage.

The moment you hire your first NEMT driver as a W-2 employee, workers' comp is legally required in nearly every state. It covers medical expenses and lost wages if a driver is injured on the job — loading a patient, operating a ramp, or slipping in a parking lot.

Discover how an all-in-one NEMT solution can automate scheduling, plan routes and simplify billing so you can focus on delivering exceptional care.

Here's the data operators actually need when building their financial models.

Source: Aggregate data from NEMT industry brokers and operator surveys, 2025–2026.

Most insurers offer monthly payment options, though you'll often pay a 5–12% financing fee if you don't pay annually.

Single sedan, new operator: $540 – $835/month

Single WAV, new operator: $750 – $1,165/month

5-vehicle mixed fleet, established: $3,500 – $6,200/month

NEMT insurance cost for a new business carries a "loss history surcharge" by default — because you have no loss history to prove you're a safe operator. Insurers typically charge 25–40% more in the first two years compared to an established operator with a clean record.

This is one reason many entrepreneurs choose to buy a NEMT business for sale rather than launch from scratch. An existing operation carries:

An established driver roster with documented records

2–5 years of verifiable loss history

Existing insurer relationships and loyalty discounts

Already-negotiated NEMT rates with brokers or Medicaid managed care organizations

For startups, expect your Year 1 premiums to be at the top end of the ranges above.

This is the question every new operator asks. The short answer: the risk profile is genuinely different.

NEMT passengers are not healthy adults who recover quickly from minor injuries. A dialysis patient with brittle bones who experiences even a low-speed collision faces a dramatically different injury outcome than a healthy commuter in the same accident. Insurers model this risk — and charge for it.

NEMT vehicles don't sit in a driveway. A single van completing 8–12 trips per day accumulates 50,000–80,000 miles per year. More miles = more exposure. Commercial auto actuaries use per-mile models to set rates, and NEMT vehicles are on the road far more than typical commercial fleets.

NEMT drivers are required to hold CPR certifications, pass background checks, and often complete defensive driving and passenger assistance training. High turnover — common in the industry — means operators are frequently onboarding new drivers, and each new driver represents an unknown risk. Insurers charge for that uncertainty.

Data: From 2022 to 2025, the average NEMT bodily injury claim settlement rose by approximately 18%, driven by medical inflation, litigation costs, and increased attorney involvement in transport-related injury cases. These trends carry directly into 2026 premiums.

Discover how an all-in-one NEMT solution can automate scheduling, plan routes and simplify billing so you can focus on delivering exceptional care.

Every state that runs a Medicaid transportation program sets minimum insurance standards for NEMT providers. Requirements vary significantly.

Always verify current requirements with your state Medicaid agency — minimums can change with contract renewals.

In states where Medicaid transportation is managed through MCOs (Aetna Better Health, Molina, Centene, etc.), the MCO contract requirements often exceed state minimums. If you're contracted with an MCO, read their credentialing packet carefully before purchasing coverage. Some MCOs require $2,000,000 per occurrence — double the state minimum.

Many new operators make a costly mistake: they purchase standard commercial auto thinking it covers their NEMT operation. It does not.

Operating a NEMT business under standard commercial auto is not only a coverage gap — it's a contract violation that can result in immediate disqualification from Medicaid brokerage programs.

Higher premiums aren't inevitable. The operators who pay the least relative to their fleet size take deliberate, documented steps to reduce risk in the eyes of underwriters.

GPS-based telematics systems that monitor speed, hard braking, and idle time give insurers real data instead of estimates. Several NEMT-focused insurers now offer telematics discount programs that can reduce premiums by 8–15% after 6–12 months of clean data. The hardware cost ($200–$500 per vehicle) pays for itself quickly.

Underwriters reward operators who go beyond minimum MVR checks. Document your hiring process: background checks, MVR pulls at hire and annually, CPR certification tracking, and defensive driving completion. Present this to your broker as part of your renewal submission.

Financing your premium through a payment plan adds 5–12% to your total annual cost. If cash flow allows, pay the full annual premium upfront. On a $40,000 annual premium, that's $2,000–$4,800 in savings.

Generalist commercial insurance brokers often place NEMT accounts with standard commercial carriers who add significant "risk loading" to unfamiliar industries. A NEMT-specialist broker has relationships with underwriters who understand the industry and price accordingly. This single change can save 10–20% at renewal.

The single biggest lever on your premium is your loss run — the claims report your insurer generates at renewal. Three consecutive years with zero or low-severity claims can qualify you for preferred-risk pricing, loyalty discounts, and access to lower-cost carriers.

Billing errors — duplicate trips, incorrect coding, unbundled services — attract audits. Audits create scrutiny. Scrutiny finds compliance gaps. Compliance gaps raise flags for your insurer. Quality NEMT billing software keeps your operation clean, which supports a clean insurance profile.

Discover how an all-in-one NEMT solution can automate scheduling, plan routes and simplify billing so you can focus on delivering exceptional care.

Whether you're launching fresh or evaluating a NEMT business for sale, insurance must be a line item in your financial model from the first draft — not an afterthought.

This works out to $3,000–$4,800/month in insurance overhead for a 3-vehicle operation. Factored against average NEMT rates of $35–$65 per one-way trip and 6–10 trips per vehicle per day, insurance represents roughly 15–22% of gross revenue in Year 1.

Year 3 Projection: With clean loss history and established driver records, the same operation typically reduces insurance to 10–14% of gross revenue — a meaningful improvement to your operating margin.

Not all brokers are created equal. When you're shopping coverage, these questions separate specialists from generalists.

Which carriers do you place NEMT accounts with? Look for names like Nationwide, Progressive Commercial, Markel, Canal, or specialty programs through Chubb or Travelers.

Do you offer telematics program access? If they don't know what you're talking about, find another broker.

Can you provide 3 loss runs from comparable operators? This helps you benchmark what clean histories look like in your state.

What's your process for MCO credentialing support? Many MCOs require certificates of insurance in specific formats.

Do you have access to programs that accept new ventures? Some carriers flatly refuse Year 1 NEMT operators.

Understanding where premiums are headed helps you plan and negotiate more effectively.

Medical Inflation: The average soft-tissue injury claim settlement rose from $14,200 in 2021 to approximately $18,700 in 2025 — a 31% increase in four years. NEMT operators bear the brunt of this trend given their passenger profile.

Reinsurance Tightening: The commercial auto market has seen reduced carrier competition. When fewer carriers compete for accounts, pricing discipline weakens and rates rise.

Medicaid Audits: Increased Medicaid audits in 2025–2026 have put compliance in the spotlight. Operators with compliance gaps are finding renewals either denied or priced at punitive levels.

NEMT insurance cost is one of the largest fixed expenses in the business. Whether you're drafting your first NEMT business plan, evaluating a NEMT business for sale, hiring your first NEMT driver, or scaling an existing fleet, you need accurate insurance projections before any other number makes sense.

Get at least three quotes from NEMT-specialist brokers. Build insurance as a percentage of revenue into your financial model. Document your driver management and safety processes from Day 1 — they directly influence what you'll pay at every renewal.

Bottom Line: The operators who treat insurance as a risk management system — not just an annual expense — consistently outperform those who don't on both premium cost and long-term profitability.

Discover how an all-in-one NEMT solution can automate scheduling, plan routes and simplify billing so you can focus on delivering exceptional care.

Q1: How much does NEMT insurance cost per month?

For a single vehicle, NEMT insurance cost per month typically ranges from $540 to $1,165 depending on vehicle type and operator history. A standard sedan or minivan for a new operator runs $540–$835/month, while a wheelchair accessible vehicle (WAV) runs $750–$1,165/month. Multi-vehicle fleets get some per-unit discount, but insurance remains one of the top two or three monthly overhead costs in any NEMT operation. Always budget for the high end in Year 1.

Q2: What is the NEMT insurance cost for a new business with no loss history?

New operators pay a premium penalty of 25–40% above market rate in their first one to two years because insurers have no loss history to underwrite against. For a single WAV, that can translate to $9,000–$14,000 annually compared to $7,000–$11,000 for an established operator with the same vehicle. The best way to minimize this gap is to present a documented driver screening process, install telematics from Day 1, and work with a NEMT-specialist broker who can access new-venture programs that standard carriers won't offer.

Q3: Why is NEMT insurance so expensive compared to regular commercial auto?

Three factors drive NEMT premiums above standard commercial auto rates. First, your passengers are medically vulnerable — a low-speed accident that causes a minor injury to a healthy adult can cause severe harm to a dialysis patient or a stroke survivor, which directly inflates claim severity. Second, NEMT vehicles log 50,000–80,000 miles per year, far exceeding most commercial fleets. Third, bodily injury settlements industry-wide have risen roughly 18% from 2022 to 2025 due to medical inflation and increased litigation. These factors combine into a significantly higher risk profile than driving construction crews or delivering packages.

Q4: Does NEMT insurance vary by state?

Yes — significantly. State Medicaid programs set minimum liability requirements that range from $1,000,000 per occurrence (Florida, Texas, Illinois) up to $1,500,000 (California). If you're contracted through a Managed Care Organization (MCO) like Molina or Centene, their credentialing requirements can push that to $2,000,000 — regardless of what your state mandates. Always verify your state's current requirements through your Medicaid agency or a NEMT-specialist broker before purchasing a policy.

Q5: How can I lower my NEMT insurance premiums?

The six most effective strategies in 2026 are:

Install GPS telematics to earn data-driven discounts of 8–15%.

Document your driver screening, MVR pull, and certification tracking processes and present them at renewal.

Pay your annual premium upfront to avoid the 5–12% financing surcharge.

Use a NEMT-specialist broker instead of a generalist.

Maintain a clean claims record for 36 consecutive months to qualify for preferred-risk pricing.

Keep your operation compliant using quality NEMT billing software to reduce audit exposure.

Q6: How Can NEMT Platform Help Operators Manage Insurance-Related Compliance?

Insurance premiums don't exist in a vacuum — they're directly tied to how well-run your operation looks to an underwriter. This is where NEMT Platform (www.nemtplatform.com) becomes a practical tool in your insurance cost management strategy.

NEMT Platform is purpose-built software for non-emergency medical transportation operators, and it addresses several of the key risk factors that insurers evaluate at renewal:

Clean Billing = Lower Audit Risk. Billing errors attract Medicaid audits. Audits surface compliance gaps. Compliance gaps are red flags at insurance renewal. NEMT Platform's billing module helps operators submit accurate, compliant claims from the start.

Driver & Trip Documentation. NEMT Platform logs driver assignments, trip confirmations, and service verifications in one place — giving you the organized records a broker needs when submitting your renewal application to underwriters.

Fleet & Trip Scheduling Visibility. When your dispatch, scheduling, and route data are centralized in NEMT Platform, you can pull clean operational reports at any time — data that some telematics programs require for premium discount applications.

Compliance Tracking. From driver certification expiration tracking to vehicle inspection scheduling, staying ahead of compliance deadlines is easier when your platform flags them automatically.

NEMT Platform doesn't replace your insurance broker — but it creates the operational infrastructure that makes your business look like a preferred-risk account. Visit www.nemtplatform.com to learn more.

Q7: Is it better to start a NEMT business from scratch or buy an existing one to save on insurance?

Buying an established NEMT business for sale can produce meaningful insurance savings in Year 1. An existing operation brings verified loss history (typically 2–5 years of clean loss runs), an established driver roster with documented records, and existing carrier relationships that carry loyalty discounts. New operators pay 25–40% more by default. That said, when evaluating a NEMT business for sale, always request 3 years of loss runs as part of your due diligence. If the existing operation has a history of frequent or high-severity claims, you may inherit a rated account — meaning you'll pay elevated premiums regardless of your own management quality until that history ages off.

Disclaimer

The rates, figures, and statistics in this article are sourced from publicly available industry data, national broker rate schedules, and general market research. They reflect national averages and broad benchmarks as of 2024-2025. Actual rates in your area may differ depending on your state, broker network, payer contracts, and local market conditions. Before setting your charge and pay structure, verify current rates directly with your state’s Medicaid broker, local MCOs, and any private insurance partners you plan to work with. This article is intended for general informational purposes only and does not constitute financial, legal, or business advice.

How NEMT billing really works in 2026: the claim lifecycle, why claims get denied, EVV and compliance, and how the right billing software gets you paid faster.

NEMT operators in 2026 can reach 20-35% margins via hospital discharge contracts, stretcher and bariatric transport, long-distance trips, and private concierge accounts beyond standard broker rides.

California is the largest Medi-Cal market in the country, with more than 14 million enrollees and a county-based managed care model that routes all NEMT trips through contracted transportation brokers, not the state directly. To run a compliant NEMT business in California, you need a CPUC Charter-Party Carrier (TCP) permit, Medi-Cal enrolment through the DHCS PAVE portal, and credentialing with the brokers serving your target counties, primarily ModivCare, MTM and SafeRide Health. Our 2026 guide covers California-specific insurance requirements under CPUC General Order 115, the Physician Certification Statement (PCS) compliance framework, the 180-day Medi-Cal FFS timely filing limit, and how to build a multi-county operation across California's fragmented broker landscape.

Discover proven NEMT marketing strategies for 2026, from local SEO to facility contracts, that help providers win high-value institutional healthcare business.